Introduction

Compared to five years ago, there have been advancements in oncology, giving rise to an improvement in patient outcomes. For people diagnosed with cancer in 2009, approximately 70% would have been alive five years later if they had had access to the novel therapeutics we have currently1. This transformation in patient outcomes can be largely attributed to increased access to innovative therapies.

Despite the evolving therapeutic area there are still several unmet needs in the oncological field, such as certain rare cancers and understudied tumour types which still lack sufficient research and treatment options. As the field of oncology is rapidly evolving, greater investment is required by manufacturers to improve the understanding of these diseases, develop targeted therapies, and to conduct clinical trials that can capture survival benefit adequately for well-managed indications. Further, innovative assessment frameworks are required that improve the evaluation of novel oncology therapeutics and mitigate payer uncertainty.

Studies in major tumour types now need to look beyond survival

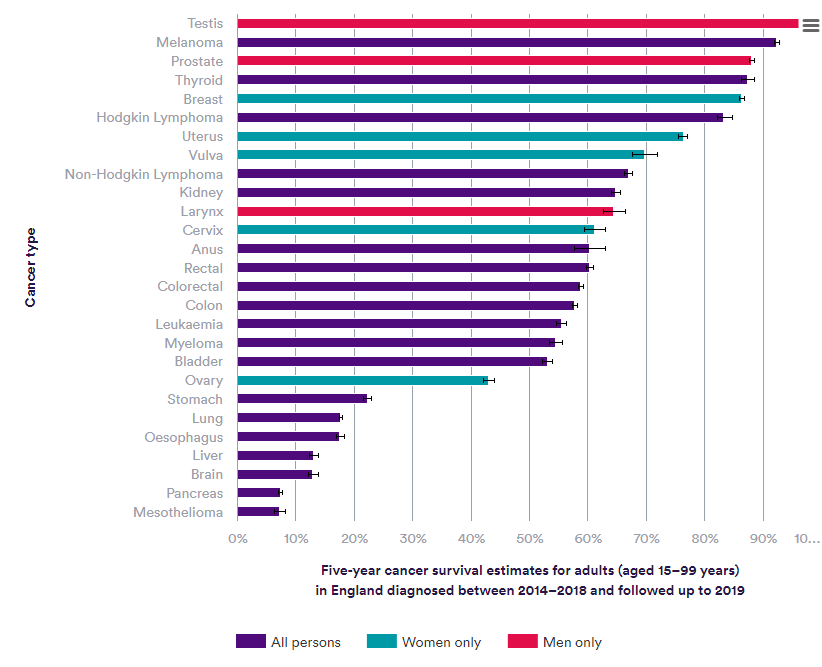

There has been extensive investment in oncology across academia and industry over the last few decades, with a targeted focus in major tumour types such as testicular cancer, melanoma of skin and breast cancer as demonstrated by respective five-year survival rates of 97%, 92.3% and 86.3%2.

Figure 1: Nuffield Trust – Cancer survival rates

In cancer, extending survival has always been the treatment goal for innovative therapies. As cancer treatments improve, the number of cancer survivors is increasing. However, survivorship issues, such as long-term side effects of treatment, psychological well-being and quality of life, need to be better addressed. Further, demonstrating survival benefit within the context of a clinical trial is increasingly difficult: it can now take more than 10 years in well-managed indications3.

Non-overall survival (OS) endpoints such as progression-free survival (PFS) and patient reported outcomes (PROs) can be captured earlier in clinical trials and can reflect broader value to patients3. Regulatory approvals are relying on non-OS endpoints for demonstration of patient benefit: between 2015 and 2020, 92% of EMA approvals for solid-tumour early-stage cancers were based on non-OS endpoints3. On the other hand, hesitancy remains amongst payers around long-term outcomes of non-OS endpoints. Consequently, their decisions remain largely driven by OS data. Irrespective of the health technology assessment (HTA) approach, immature OS data can lead to increased uncertainty, increase in time to a decision and subsequently increase in time to patient access. Therefore, as treatment outcomes are improved, and some cancer indications are starting to be managed as chronic diseases there is an urgent need to address survivorship issues and mitigate payer concern to improve acceptance of non-OS endpoints.

The evolving oncological field needs to focus on rare cancers

Several tumour types still lack sufficient research and treatment options. A study from the University of Pennsylvania revealed that up to 50% of cancer-signalling proteins previously thought to be immune to therapeutic treatment may be treatable4. In this study researchers identified hidden protein targets, believed to be a promising target for cancer therapy providing new opportunities for developing drugs.

Treatment outcomes for rare cancers such as B cell and plasma cell malignancies have improved remarkably due to the use of chimeric antigen receptor (CAR) therapies, a type of immunotherapy. Over the last decade data demonstrate that CD19-targeted CAR T cells can induce prolonged remissions in patients with B cell malignancies, often with minimal long-term toxicities, and are probably curative for a subset of patients5.

The success of CAR-Ts in haematological cancers is driving the development of more advanced immune cell therapies, which hold promise for their indication to treat solid cancers and non-malignant diseases in the future6. Pancreatic cancer currently has a survival rate of just 7.3%2. CAR-T cell therapies that target Claudin-18.2, a common molecular target in pancreatic cancer, have demonstrated a disease control rate of 73% and overall response rate of 48.6%6. Continued investment from industry is necessary to improve treatment outcomes for rare cancers and understudied tumour types.

Assessment criteria must capture unique value of immunotherapies

From a market access perspective, an unmet need is the ability of HTA bodies to evaluate the value of oncology immunotherapies, therefore advancement in assessment methodologies is required to keep up with the evolution of pharmaceutical oncology efforts, specifically extended survival rates and non-OS endpoints. Limitations of current value assessment frameworks such as the evaluation of side-effects, which are often increased with immunotherapies, and aforementioned survivorship issues prevent payers, patients, and physicians from understanding the long-term value of these novel therapeutics. For instance, patients receiving the combination therapy of Opdivo and Yervoy reportedly developed side-effects which were resolved within the next 4-6 weeks, but existing frameworks did not account for the improvement of these side-effects or the potential long-term PFS of their use7.

To address these methodological challenges in appraising new therapeutics, a shift in assessment criteria that reflects market-access considerations of novel oncology therapeutics is required. One solution could involve the implementation of evidence generation frameworks to collect data on the incremental benefits. This further evidence generation can help to mitigate payer uncertainty and align a therapeutic’s value proposition with its price tag. Innovative assessment frameworks can also improve payer acceptance to the use of PROs and non-OS endpoints, which can improve the evaluation of a therapeutics clinical value and survival benefit to the patient and physician.

Conclusion

The existence of several unmet needs in oncology means that despite, the progress in treatment advancement in recent years, there remains opportunity for manufacturers to address unmet needs in the oncological field.

Investment in major tumour types such as breast cancer has seen major advancements in treatment outcomes, but limitations of clinical trials to capture this survival benefit now need to be addressed. Further, rare cancers and understudied tumour types need investment to ensure treatment outcomes can be improved for these indications too. The development of more advanced oncology immunotherapies is holding promising potential to target novel therapeutic targets. However, to address the unmet clinical and research needs in oncology, there is a need for innovative assessment frameworks on the regulatory and market access front to ensure that the value of novel oncology therapeutics is recognised in assessment criteria and patients can access these treatments.

Source:

- Cancer. Our world in data. https://ourworldindata.org/cancer Accessed 20th June 2023.

- Cancer survival rates. Nuffield Trust https://www.nuffieldtrust.org.uk/resource/cancer-survival-rates Accessed 20th June 2023.

- Looking beyond survival. ISPOR Webinar December 2022. https://www.ispor.org/conferences-education/education-training/webinars/webinar/looking-beyond-survival-data-understanding-the-value-of-non-os-endpoints-in-oncology-reimbursement-decision-making

- Penn Medicine Research Suggests More Cancers Can Be Treated with Drugs Than Previously Believed. Penn Medicines News March 2023. https://www.pennmedicine.org/news/news-releases/2023/march/penn-medicine-research-suggests-more-cancers-can-be-treated-with-drugs-than-previously-believed

- Cappell, K.M., Kochenderfer, J.N., 2023. Long-term outcomes following CAR T cell therapy: what we know so far. Nature Reviews Clinical Oncology 20, 359–371.. https://doi.org/10.1038/s41571-023-00754-1

- Labanieh L, Mackall CL. CAR immune cells: design principles, resistance and the next generation. Nature. 2023 Feb;614(7949):635-648. doi: 10.1038/s41586-023-05707-3. Epub 2023 Feb 22. PMID: 36813894.

- Henriques, C. (2017). Immunotherapy Needs New Value Framework, Say SITC 2016 Attendees. Retrieved from https://immuno-oncologynews.com/2017/02/14/immunotherapy-may-need-to-have-its-own-value-model/